ERC Action Center

In 2025, the HIRE Coalition led a national advocacy effort to prevent a retroactive termination of the entire ERC program. The HIRE Coalition was the first group to identify the Byrd Rule as a way to prevent this outcome and successfully advocated for a limited repeal, saving small businesses billions of dollars.

However, our work is not done. Tens of thousands of ERC claims remain pending. Although the IRS has long-since stopped updating ERC backlog figures, reports from the National Taxpayer Advocate (NTA) and Government Accountability Office (GAO), along with testimony from IRS CEO Frank Bisignano, provide some insight into the backlog. Here is a timeline of key updates over the last year:

ERC timeline

- May 2025 NTA blog: 597,000 claims in backlog; 84,000 disallowance letters issued[1]

- Note: we believe this number does not fully capture all PEO-related claims.

- June 2025 NTA report: IRS on pace to clear backlog by end of 2025[2]

- February 2026 GAO report: IRS closed all remaining ERC claims, except those under exam or Appeals, by December 31, 2025; 41,000 claims in exam or Appeals[3]

- March 4, 2026: IRS CEO testifies that less than 29,000 claims remain and all are in compliance[4]

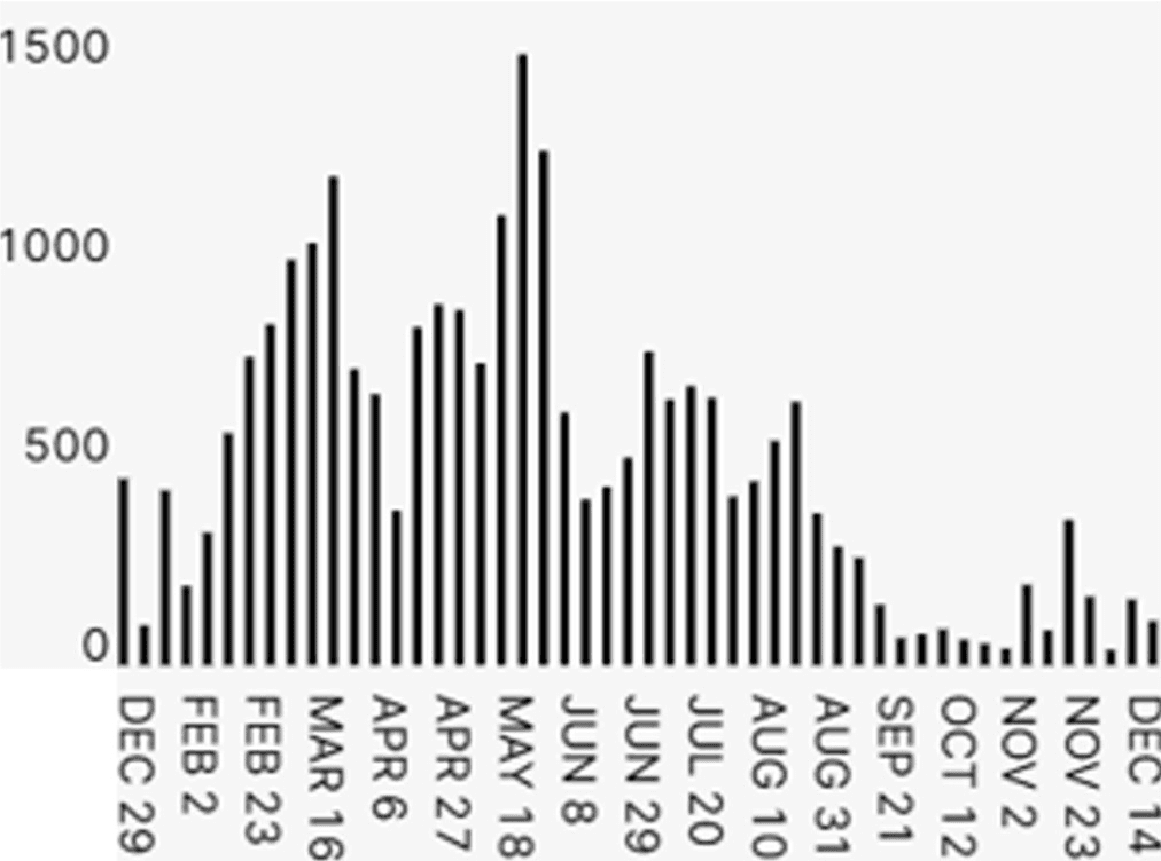

The June 2025 NTA report states that the IRS processed a record 395,000 claims between January and April 2025. The report stated if the IRS kept up that same processing rate it would clear the backlog by the end of 2025. However, the IRS did not keep up that same processing rate. This chart from TaxNow, which monitors thousands of ERC claims through IRS transcripts, shows the rate of ERC processing from December 29, 2024 through December 14, 2025.

As you can see, ERC processing rates fell off dramatically in the second half of 2025. Analysis of ERC processing statistics in the June 2025 NTA report and the NTA's January 2026 Annual Report to Congress – 2025[5] also indicate the IRS's processing rate slowed in the second half of 2025 and that a considerable backlog remains. As mentioned above, the IRS processed 395,000 claims between January and April 2025. Per the January 2026 NTA report, the IRS processed 799,000 total ERC claims in CY 2025. Based on these numbers, the IRS processed 404,000 claims between May and December 2025. If there were 597,000 ERC unprocessed claims as of April 15, 2025 and the IRS processed 404,000 claims between May and December, the backlog of ERC claims would be approximately 193,000. Based on these data points, it seems very unlikely that the IRS closed all ERC claims (except for those in audit or Appeals) by December 31, 2025.

In February 2026, the HIRE Coalition conducted its own survey to estimate the number of small businesses with unprocessed ERC claims. Based on the survey response, HIRE estimates that the backlog of unprocessed ERC claims as of February 2026 could be as high as approximately 270,000. In this context, “unprocessed” means the IRS has not issued a disallowance letter or selected the claim for exam. These unprocessed claims are in addition to tens of thousands of claims currently sitting in exam, awaiting a response to a protest of the disallowance letter, or in Appeals.

In addition to the pending claim backlog, there is also a backlog of ERC protests and appeals. Thousands of taxpayers followed the IRS's instructions to protest a disallowance notice[6], but the IRS has yet to respond to many protests. The NTA's Annual Report to Congress – 2025 paints a sobering picture on the outlook for these claims:

In the summer of 2024, the IRS issued about 28,000 ERC disallowance notices after running the claims through its risk scoring analysis. Because these claims were not previously examined, IRS examiners are now reviewing the protests before transferring them to Appeals. Practitioners report that these protests remain unaddressed and stalled in IRS inventory. At the same time, the notices of claim disallowance that the IRS issued in the summer of 2024 are coming up on the [IRC Section 6532] two-year expiration within months, yet the IRS has not assigned many of these administrative protests to Appeals. The IRS already rejected 316 taxpayer ERC protests because the two-year deadline expired. Without immediate steps to improve the Form 907 process, this number is sure to increase, as tens of thousands of taxpayers risk losing their administrative appeal rights, being forced into premature litigation, or permanently forfeiting their refunds.[7]

Even when a disallowed claim is assigned to Appeals, practitioners report that hearings take several months to be scheduled and resolved. Thus, there is no guarantee that Appeals will be able to adjudicate the claim before the two-year period expires. In short, thousands of taxpayers are running out of time, and many will end up in litigation absent the IRS approving an extension via Form 907.

Recently, Senators Crapo and Wyden introduced the Taxpayer Assistance and Service (TAS) Act, which would fix this issue by suspending the two-year limitation where a claim is pending before Appeals. However, this change would only apply to claims received after enactment and, therefore, not help ERC claimants. In light of the issues described above, the HIRE Coalition urges Congress to revise the TAS Act to include all claims currently pending before Appeals and, in the interim, encourage the IRS to take the following steps:

- Publish updated ERC processing statistics.

- Update all taxpayers regarding the status of their ERC claims.

- Issue disallowance letters to any claims that it has “closed” so taxpayers can protest and/or appeal the IRS's determination.

- Ensure all documents uploaded via the Document Upload Tool (DUT) are timely processed.

- Timely approve all ERC-related Form 907 requests.

References

- See NTA Blog, “The ERC Claim Period Has Closed – The IRS Must Now Prioritize Resolution, Communication, and Taxpayer Protections,” May 8, 2025, available at taxpayeradvocate.irs.gov. ↩

- See NTA, “Objectives Report to Congress – Fiscal Year 2026,” June 2025, available at taxpayeradvocate.irs.gov (PDF). ↩

- See GAO, “COVID-19 Relief: IRS Can Use Lessons Learned to Address and Prevent Improper Payments in Future Tax Programs,” February 2026, available at files.gao.gov. ↩

- See testimony of IRS CEO, Frank J. Bisignano, before the Full House Ways & Means Committee, March 4, 2026, available at waysandmeans.house.gov. ↩

- See NTA, “Annual Report to Congress – 2025,” January 28, 2026, available at taxpayeradvocate.irs.gov. ↩

- See IRS, “Understanding Letter 105-C, Disallowance of the Employee Retention Credit (ERC),” last updated October 15, 2025, available at irs.gov. ↩

- See Endnote V at pages 14-15. Page 9 of the NTA's report indicates that 83,000 disallowance letters had been issued by August 30, 2024. ↩